FedNow: Decoding the Latest Entry into the Fintech Space

Will FedNow instant payments replace checks?

Can real-time payment services like FedNow eat into the share of checks and ACH?

Looks very likely! Deloitte predicts that instant payments will divert up to $37 trillion from checks and ACH in the US by 2028.

FedNow is the Federal Reserve’s initiative to boost real-time payments. In this blog, we look at the impact FedNow will have on B2B payments.

What is FedNow? 🏦

FedNow is an instant payment service developed by the Federal Reserve to enable businesses and individuals to send and receive payments within seconds. This service is available 24/7/365.

Launched in July 2023, this is the only government-regulated instant payment service available in the US. Fifty-seven financial institutions and service providers including JP Morgan Chase, Wells Fargo, U.S Bank, and Finastra are part of this platform.

FedNow utilizes the ISO 20022 payment messaging standard and IBM’s MQ Client library to support the exchange of messages between participants. It also provides API access to promote easy connectivity and continued innovation in the instant payments market.

FedNow vs. ACH vs. Wire Transfer vs. RTP 💳

Though the fintech landscape is an ever-evolving one with many innovative payment mechanisms such as digital wallets, e-currencies, etc., B2B businesses tend to rely more on traditional methods.

Checks continue to be the most common means for B2B payments (47%), followed by ACH (34%) and wire transfers (13%). With more businesses shifting to paperless workflows, we can expect to see the use of electronic payment options such as ACH and instant payments rise.

The usage of checks has declined by almost 50% in the last 15 years and we expect it to reduce further as real-time payments become more widespread.

Here’s a quick comparison of the different payment types:

Will FedNow revolutionize receivables management? 🔄

When NACHA released its same-day ACH transactions in 2016, only 6% of the first 2 million transactions were B2B payments.

There is a general hesitancy among businesses in adopting real-time payments. CFOs plan their working capital management by aiming to float their capital for a longer period. The longer payment processing time of checks and ACH payments allows them to keep cash in hand for longer.

Hence, even if most businesses offer FedNow as a payment option, B2B customers may likely not be eager adopters.

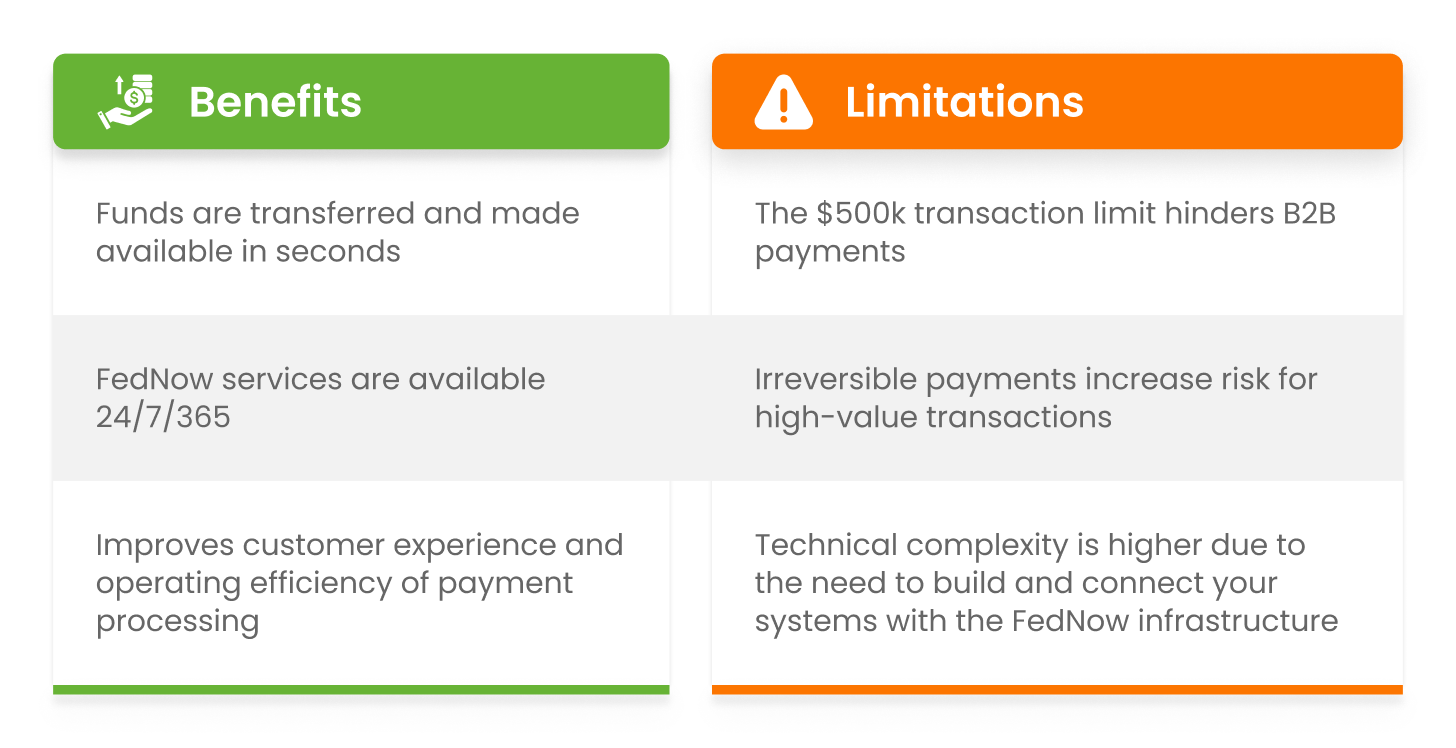

Here’s a quick look at the benefits and challenges of using FedNow for B2B payments.

That said, the ease of real-time payments and their lower processing charges will help drive higher adoption in the coming 2-5 years.

The key drivers of a transition to instant B2B payments 🔑

While the transition to real-time electronic payments may not happen overnight, there are several factors that’ll eventually boost the adoption rates. Here we discuss some of them.

Better payment experience: 47% of US finance executives believe creating a B2B payment experience similar to P2P payments is an important transformation needed.

Easier payment reconciliation: Many RTP systems including FedNow use ISO 20022 messaging standards that enable faster account reconciliation.

Lower costs: FedNow service charges per transaction are much lower than those of ACH and wire transfers.

Better visibility: The speed of real-time payments will give businesses the flexibility to pay and receive payments closer to the due date. Improved transaction reporting supports real-time visibility into account balances.

Conclusion

Countries like Brazil and India make several billion dollars of transactions every day through instant payment platforms.

The adoption of FedNow and other instant payment platforms in the US, especially among B2B businesses, will be gradual.

FedNow is not going to be a complete replacement for existing payment channels. But it will eat into the share of checks and ACH transfers in the next 2 - 5 years because of its speed of processing, lower costs, and reliability.

This quote from Eric Segal, MD at CFO Consulting Partners, sums up what finance leaders feel about FedNow today.

Read the full article here: Link